All Categories

Featured

Table of Contents

Dear Liz: When is the "sweet area" for me to begin receiving Social Security benefits? I am retired and collecting 2 government pensions mine and my ex-husband's. I paid into Social Safety and security for 26 years of considerable incomes when I was in the economic sector. I do not intend to return to work to reach 30 years of significant profits in order to prevent the windfall removal stipulation decrease.

I am paying all of my costs presently yet will certainly do more taking a trip once I am accumulating Social Security. I assume I require to live until concerning 84 to make waiting a great choice.

If your Social Safety and security benefit is genuinely "enjoyable money," as opposed to the lifeline it acts as for the majority of people, maximizing your benefit might not be your leading priority. However obtain all the details you can about the cost and advantages of declaring at various ages prior to making your choice. Liz Weston, Certified Financial Coordinator, is a personal money columnist for Concerns may be sent out to her at 3940 Laurel Canyon Blvd., No.

Cash value can build up and grow tax-deferred within your policy. You might utilize those funds for a selection of objectives later on, including supplemental retirement income, education funding or to assist pay the recurring expenses in your plan. This can be achieved via plan loans or withdrawals. However, it is necessary to note that superior policy fundings build up interest and lower cash worth and the survivor benefit.

Nevertheless, if your cash money value fails to grow, you might need to pay higher premiums to keep the policy active. Policies might provide different options for growing your cash worth, so the crediting price depends upon what you select and how those alternatives carry out. A fixed sector earns interest at a specified price, which may alter gradually with financial conditions.

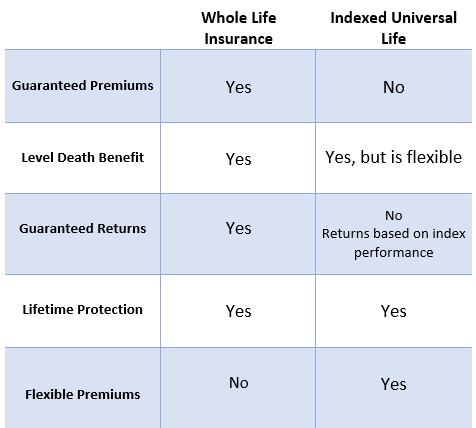

Neither kind of policy is necessarily much better than the other - it all comes down to your goals and approach. Entire life policies may appeal to you if you favor predictability. You understand exactly just how much you'll need to pay each year, and you can see just how much cash money value to anticipate in any given year.

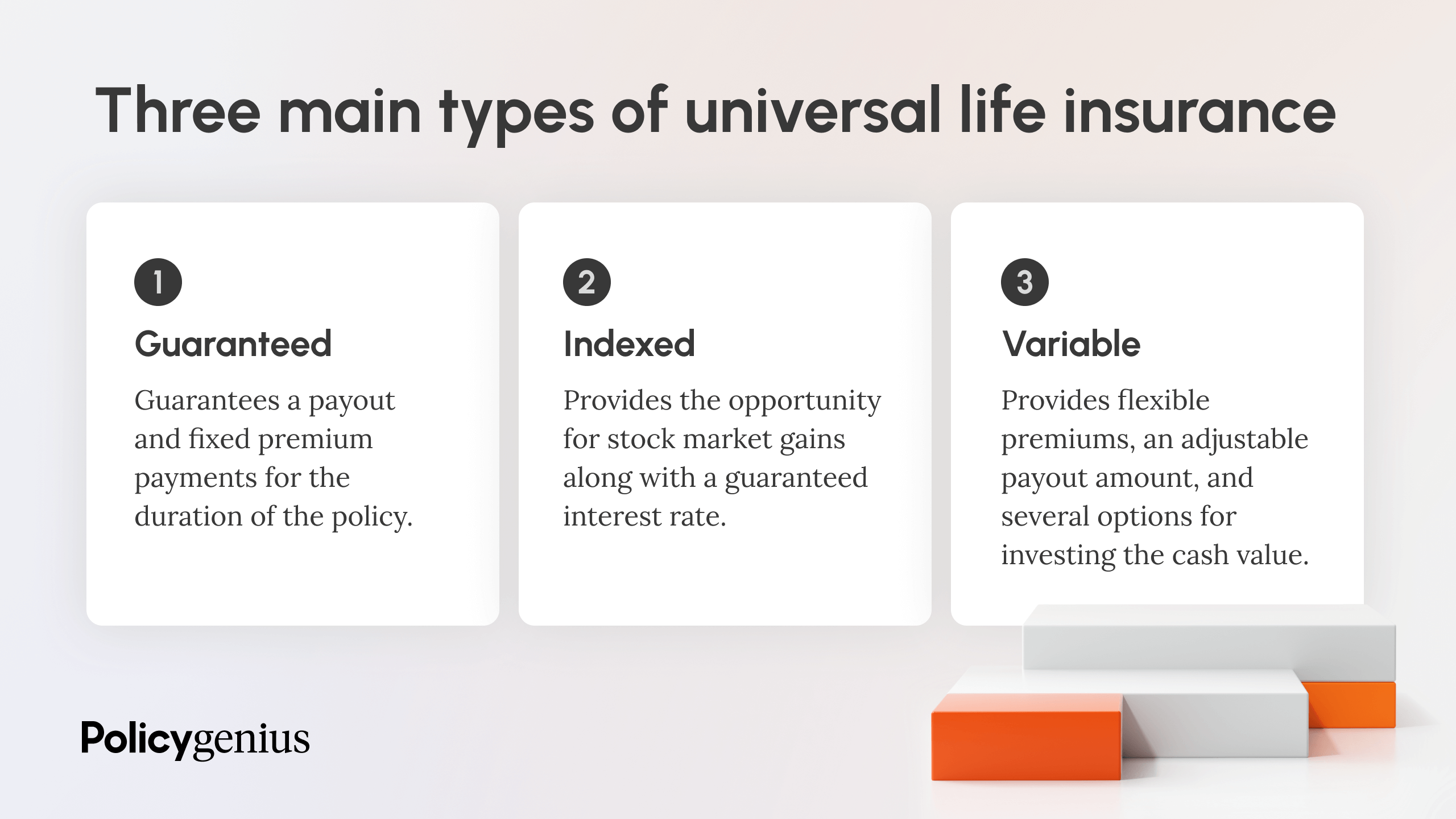

Equity Indexed Universal Life Insurance Contracts

When assessing life insurance needs, examine your long-lasting goals, your current and future expenses, and your desire for safety and security. Discuss your objectives with your agent, and choose the plan that functions best for you. * As long as required premium payments are prompt made. Indexed Universal Life is not a protection investment and is not an investment in the market.

Last year the S&P 500 was up 16%, but the IULs growth is topped at 12%. 0% floor, 12% possible! These IULs ignore the existence of rewards.

Using Iul For Retirement

Second, this 0%/ 12% video game is generally a shop technique to make it seem like you always win, but you don't. 21 of those were greater than 12%, averaging almost 22%.

If you need life insurance coverage, get term, and invest the rest. -Jeremy by means of Instagram.

Your present browser could limit that experience. You might be using an old browser that's unsupported, or settings within your web browser that are not suitable with our website.

Currently using an updated browser and still having trouble? Please give us a call at for further aid. Your present web browser: Discovering ...

Index Universal Life Vs Roth Ira

You will certainly have to give specific information regarding yourself and your lifestyle in order to obtain an indexed universal life insurance policy quote. The insurance firm might ask for info like your day of birth, gender, height, weight and whether or not you're a cigarette smoker. Smokers can expect to pay greater premiums forever insurance than non-smokers.

Mortality Charge For Universal Life Policies

If the policy you're looking at is generally underwritten, you'll need to finish a clinical test. This test includes meeting with a paraprofessional who will certainly obtain a blood and urine sample from you. Both samples will certainly be examined for possible health and wellness risks that might impact the sort of insurance coverage you can obtain.

Some factors to think about include the amount of dependents you have, the amount of revenues are entering your family and if you have expenses like a home loan that you would desire life insurance policy to cover in case of your fatality. Indexed global life insurance policy is among the a lot more complex sorts of life insurance policy currently available.

If you're looking for an easy-to-understand life insurance policy, however, this may not be your ideal option. Prudential Insurance Provider and Voya Financial are several of the most significant providers of indexed global life insurance. Voya is taken into consideration a top-tier supplier, according to LIMRA's 2nd quarter 2014 Final Costs Coverage. While Prudential is a historical, very valued insurance provider, having actually stayed in business for 140 years.

Indexed Universal Life Insurance Definition

On April 2, 2020, "A Critical Testimonial of Indexed Universal Life" was made readily available through numerous outlets, including Joe Belth's blog site. Not surprisingly, that piece generated considerable comments and objection.

Some dismissed my remarks as being "brainwashed" from my time helping Northwestern Mutual as a home workplace actuary from 1995 to 2005 "regular entire lifer" and "biased against" products such as IUL. There is no disputing that I functioned for Northwestern Mutual. I enjoyed my time there; I hold the business, its staff members, its products, and its shared approach in high respect; and I'm grateful for all of the lessons I learned while employed there.

I am a fee-only insurance coverage consultant, and I have a fiduciary obligation to keep an eye out for the very best passions of my clients. Necessarily, I do not have a bias towards any type of product, and in reality if I find that IUL makes good sense for a client, then I have a commitment to not just existing but recommend that alternative.

I constantly strive to place the most effective foot ahead for my customers, which indicates using designs that reduce or eliminate compensation to the best level possible within that certain policy/product. That does not constantly indicate recommending the plan with the least expensive settlement as insurance is much more challenging than just contrasting compensation (and occasionally with items like term or Ensured Universal Life there just is no commission versatility).

Some suggested that my degree of enthusiasm was clouding my reasoning. I like the life insurance policy industry or a minimum of what it might and should be (is indexed life insurance a good investment). And of course, I have an unbelievable amount of interest when it concerns really hoping that the market does not obtain yet one more black eye with extremely optimistic pictures that established consumers up for disappointment or worse

Columbia Universal Life

And now history is repeating itself once more with IUL. Over-promise now and under-deliver later. The even more things alter, the even more they remain the very same. I might not have the ability to alter or save the industry from itself relative to IUL products, and frankly that's not my objective. I desire to aid my customers make best use of worth and prevent vital errors and there are consumers out there every day making poor decisions with regard to life insurance policy and especially IUL.

Some people misunderstood my objection of IUL as a covering endorsement of all things non-IUL. This could not be further from the fact. I would not directly suggest the vast majority of life insurance policy policies in the market for my customers, and it is unusual to find an existing UL or WL plan (or proposition) where the presence of a fee-only insurance coverage expert would not add considerable client worth.

{kind=link}

Latest Posts

Universal Life Policy Pros Cons

Iul Tax Free Retirement

Guaranteed Universal Life Insurance Quote